VAT Withholding

What is VAT Withholding?

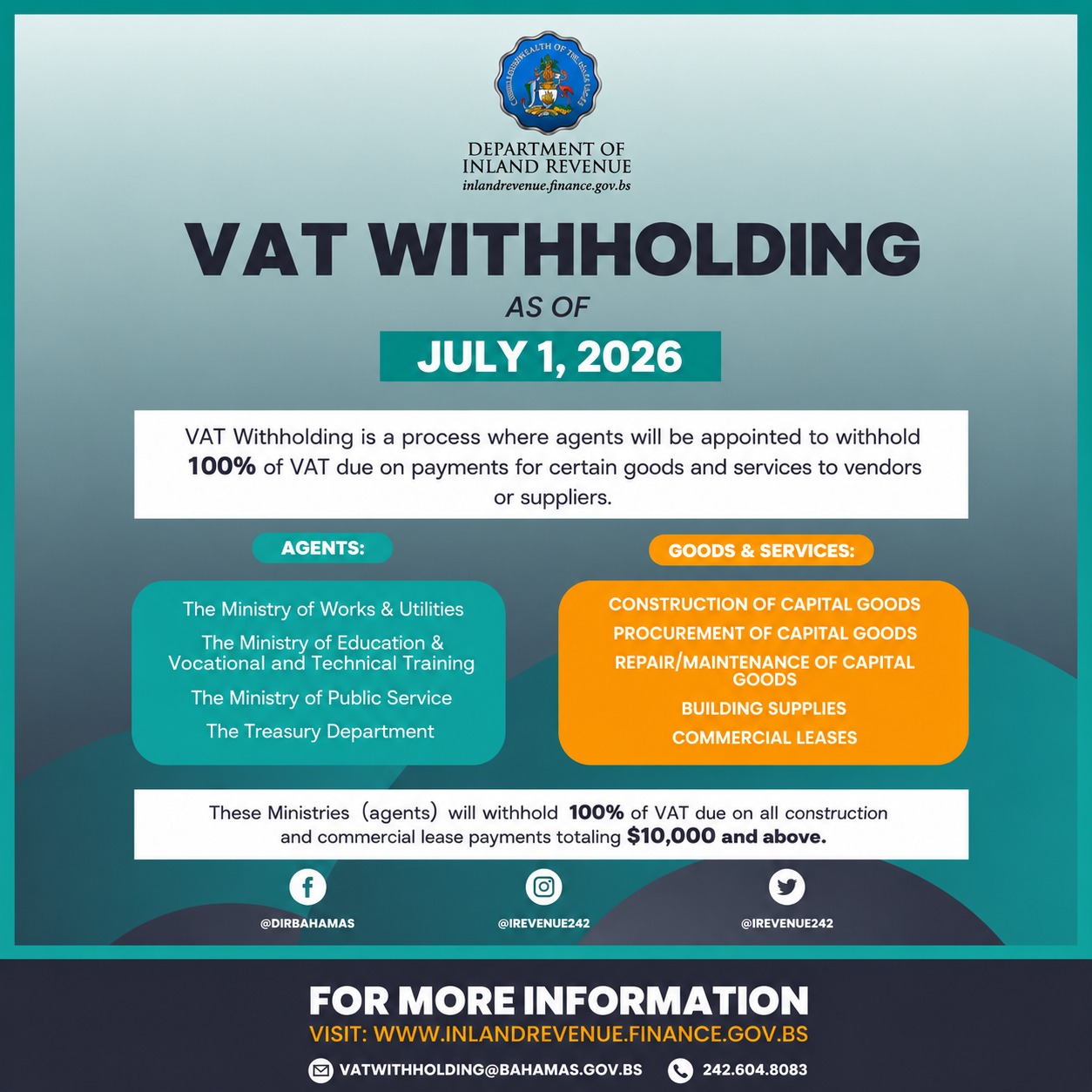

Withholding VAT is an administrative mechanism that requires certain VAT registrants or government agencies (called VAT Withholding Agents) to withhold and remit to the government 100% of the VAT due on payments to its vendors. This withholding is not a tax, but rather an alternative accelerated method of collecting VAT due by suppliers (vendors). This provision only applies to supplies that attract the standard (10%) VAT rate.

The Public Treasury, the Ministry of Works and Utilities, the Ministry of Education and Vocational and Technical Studies, and Ministry of the Public Service were appointed as VAT Withholding Agents on July 1st, 2022, and are required to withhold 100% of the VAT from all payments above $9,999.99.

In the future, there may be other government entities and private businesses appointed as Withholding Agents.

Agent’s Certificate of Registration (Form 72)

How does withholding VAT work?

Assume that the VAT Withholding Agent purchases construction services or rents an office space from a VAT registered supplier named John. John’s contract was for $100,000 before VAT. When the job was done, John gives the Withholding Agent an invoice for $100,000 plus $10,000 of VAT, for a total of $110,000.

When the Withholding Agent pays the invoice, they will pay John $100,000, and provide him with a Withholding VAT Certificate showing that the $10,000 VAT has been withheld. This VAT is remitted directly to DIR on John’s behalf.

Click the link below for VAT Withholding Certificate

VAT Withholding Certificate (fillable)

Click here to view the Guidance on VAT Withholding (Coming soon)